Busting super myths

With $2.9 trillion* invested, Australia’s super system is routinely ranked among the top retirement systems globally. Given its reputation, it’s no wonder people like to talk about super.

Unfortunately, some of the things people say and hear about super aren’t always correct. To help you separate fact from fiction, we’ve busted a couple of common super myths:

I can nominate any friend or family member as a beneficiary

It depends. Legally, your super is designed to be passed to your dependants. A dependant can be your:

- Spouse: incudes married, de facto, and same sex

- Children: Includes biological, step, adopted, ex-nuptial, or your spouse’s children

- Financial dependent: A person wholly or partially financially dependent on you

- Interdependent: A person who you live with in a close personal relationship, where one or both provide financial support and domestic support, or personal care. Other circumstances may also apply.

So, if you make a binding nomination to an individual, they must fit into one of those categories.

If you want to leave your super to someone who doesn’t fit into one of those categories, such as a friend or charity, you can make this specification in your will, and then nominate your legal personal representative as your beneficiary. Your legal personal representative is the legal executor of your will, or the person responsible for your estate.

Watch this short video to learn more about the different types of beneficiaries:

I pay tax on my super

Tax on contributions

Before-tax contributions to your super are taxed at 15%. This includes the compulsory contributions your employer makes, as well as any salary sacrifice contributions you make.

Tax on earnings

Tax is applied to the investment earnings in your super account at a rate of 15%, and reflected in our credited interest rates (CIRs). However, investment earnings in an income account are tax-free if you are a Retirement Member.

Tax on withdrawals

If you are eligible and choose to withdraw money from your super before you turn 60, you will pay tax on any amounts you withdraw. Meanwhile, if you take any part of your super in cash after age 60, generally no tax is payable.

I can buy a house with my super

This one is a bit tricky – it’s not exactly a myth, but while you can technically buy a house with your super, it’s likely not as easy as you think. In particular, the answer depends heavily on who you are, and what type of house you are looking to buy and why.

There are two main ways in which your super could help you buy a house:

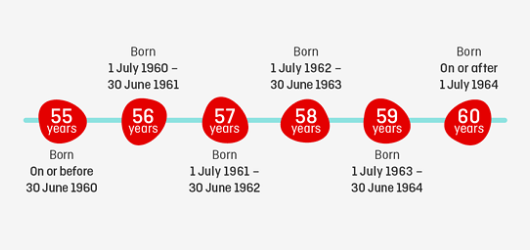

I have to wait until I'm 67 to access my super

No. If you satisfy a condition of release, you may actually be eligible to start accessing your super when you hit what’s called your ‘preservation age’. This depends on the year were born:

If you’ve heard age 67, it may be in relation to the Age Pension, which you may be able to begin accessing (if you’re eligible) when you hit your ‘qualifying age’. Like your preservation age, this depends on the year you were born:

Was this helpful?

We're here to help

If you want to learn more or need help with making a decision about your super, you can get simple advice over the phone. It’s included as a part of your membership so there’s no extra cost.