Investment insights: December 2023 quarter

Qantas Super had a strong end to the 2023 calendar year, with each of our investment options posting strong gains over the December quarter.

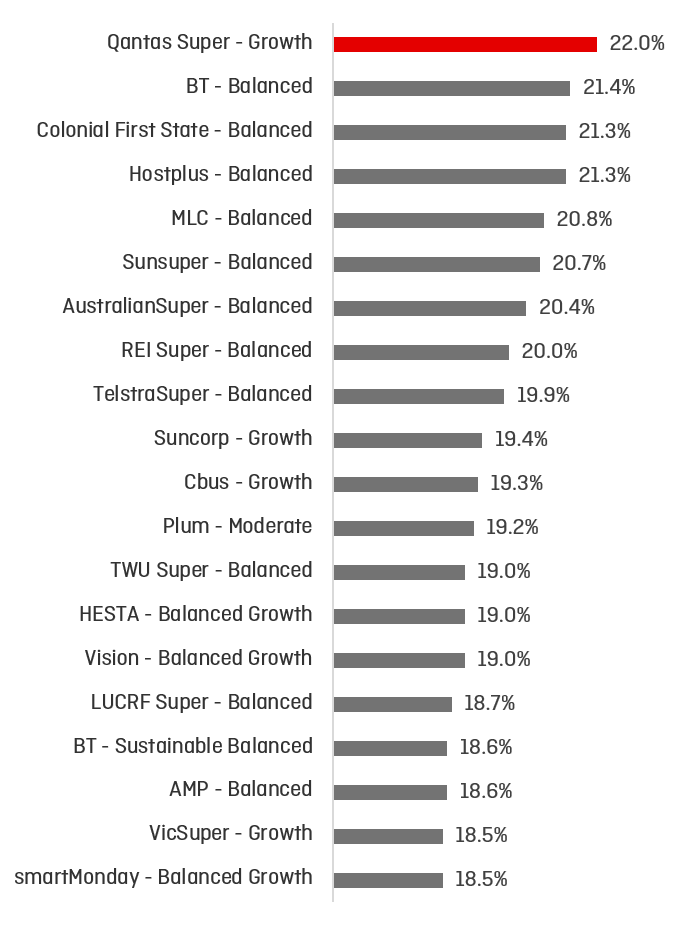

Qantas Super’s Growth option has been ranked the top balanced option for the 2020/21 financial year by leading independent research house, SuperRatings.

This excellent performance was seen across the board, with all of our investment options performing exceptionally well over the 2020/21 financial year. In fact, both our Aggressive and Growth options have realised the highest returns for a Qantas Super option since 1987, with Aggressive returning 26.8% and Growth returning 22% over the 2020/21 financial year.

For Retirement Members with an Income Account the news is even more positive with Aggressive returning 29.5% and Growth returning 24.2% for the 2021/21 financial year.

Each of the four stages in Glidepath, our lifecycle investment strategy, delivered their best returns to date since Glidepath launched in 2015.

Our Chief Investment Officer, Andrew Spence said Qantas Super is proud to be a fund that members can continue to rely on to deliver strong performance.

“With so many of our members facing uncertainty over the last year, it was more important than ever to ensure that our investment options lived up to their performance objectives. Our aim is to help members feel confident in their financial future so they can enjoy retirement, and a key factor in instilling confidence is strong investment performance, so we’re proud to have delivered these excellent returns.”

Annual returns to 30 June 2021

Source: SuperRatings. Returns are after investment fees. Past performance is not an guarantee of future performance.

| Investment option | Super and TTR accounts | Income accounts |

|---|---|---|

| Glidepath: Take-off | 26.9% | 29.5% |

| Glidepath: Altitude | 22.0% | 24.2% |

| Glidepath: Cruising | 18.2% | 20.3% |

| Glidepath: Destination | 15.4% | 17.0% |

| Aggressive | 26.8% | 29.5% |

| Growth | 22.0% | 24.2% |

| Balanced | 15.3% | 17.0% |

| Conservative | 9.8% | 11.1% |

| Cash | 0.7% | 0.9% |

Returns are after investment fees. Past performance is not a guarantee of future performance.

The results for the 2020/21 financial year highlight the importance of investing your super for the long term.

While it’s natural to feel unsettled when there’s significant volatility in global financial markets, as we saw when the COVID-19 pandemic began to spread in the March 2020 quarter, volatility is a normal part of investing for the long term.

However, Qantas Super’s safety-first approach to investing means your super is designed to weather any storm. We protect your super by investing for the long-term and building well diversified portfolios with investments that complement each other.

This approach allows us to both protect your super through periods of market uncertainty, as well as capitalise on periods of growth. So, while it may be tempting to change your strategy when you see share markets falling, in the long run it can make more sense to either stay invested or consider investing more. This is the sort of decision a Super Adviser can help you with.

By changing to a lower risk option in a downturn, you risk selling out at a time when prices are low, rather than taking advantage of falls when markets recover, as they did through 2020/21.

In fact, after a year to forget, markets rebounded remarkably quickly: the benchmark S&P/ASX200 index, for example, rose 24 percent over the financial year, marking its biggest gain since its inception. The rebound was buoyed by factors including central banks lowering interest rates, governments around the world providing stimulus, and the rapid development of COVID-19 vaccines.

Our defined benefit asset pool, which is invested via a specialised investment strategy, also saw strong performance over the 2020/21 financial year, delivering a return of 13.5%.

According to Qantas Super investment manager Chris Grogan, this specialised strategy must balance Qantas Super’s defined benefit liabilities both now, and decades into the future. For example, he explained, if every member’s defined benefit component were to be crystallised today, we must be able to pay out every member’s benefits today.

Of course, in reality, these defined benefit components will crystallise one by one over the decades to come. And, because these benefits are calculated according to a formula that takes into account factors including a member’s Credited Service and their salaries in the years leading up to crystallisation, our investment strategy must also look to the long-term, catering for how these variables will change over time.

Our defined benefit liabilities and the defined benefit pool are monitored by our Plan Actuary, who monitors defined benefit funding and the appropriateness of the investment strategy.

The defined benefit pool had a significant surplus of $234 million as at 31 March 2021. This surplus meant the pool was 10.7% overfunded relative to member obligations.

Qantas Super had a strong end to the 2023 calendar year, with each of our investment options posting strong gains over the December quarter.

Markets kicked off the 2023 calendar year on a positive note, with each investment option almost doubling their return for the year to date from the December 2022 quarter to the end of March 2023.

After several years of volatility in investment markets, with returns swinging from negative to record highs, and back to the low single-digits, the 2022/23 financial year has seen a return to what we could consider more ‘normal’ numbers, with Qantas Super delivering strong absolute returns across all investment options.