Investment insights: December 2023 quarter

Qantas Super had a strong end to the 2023 calendar year, with each of our investment options posting strong gains over the December quarter.

You’ve probably heard it dozens of times already, and you’ll hear it dozens more: super is a long term investment, and volatility is a normal part of investing for the long term.

But we know it’s one thing to hear that when your balance keeps going up, and you get to imagine just how much it will keep growing over that long term. It’s another altogether when you see a drop in your balance from one day to the next as a result of significant volatility, like we’re seeing now.

So, why do we keep talking about the long term?

While past performance is not an indicator of future performance, Qantas Super investment manager Chris Grogan said a hundred years of trends give us a good indication of where the market will likely go from here.

From the crash of 1929 to that of 1987, and to the recession Paul Keating said we “had to have”, markets have always recovered.

In fact, the recovery from the recession of 1991 saw Australia record almost 30 years of consecutive growth. This was the longest stretch of growth without a recession for any country in the developed world since World War II.

More recently, in our December quarter market update we looked at how the ASX reached a record peak of 7,041.4 points in January, after reaching its pre-global financial crisis peak in July 2019.

Along with reminding us that markets do eventually recover, these past events can serve as a reminder that by changing to a lower risk option in a downturn, you risk crystallising your loss by selling out at a time when prices are low.

Let’s look at it in terms of buying and selling a house: if you bought a house for $1 million, and then house prices dropped and your home was valued at $750,000, you would only make a loss if you actually decided to sell it at this point.

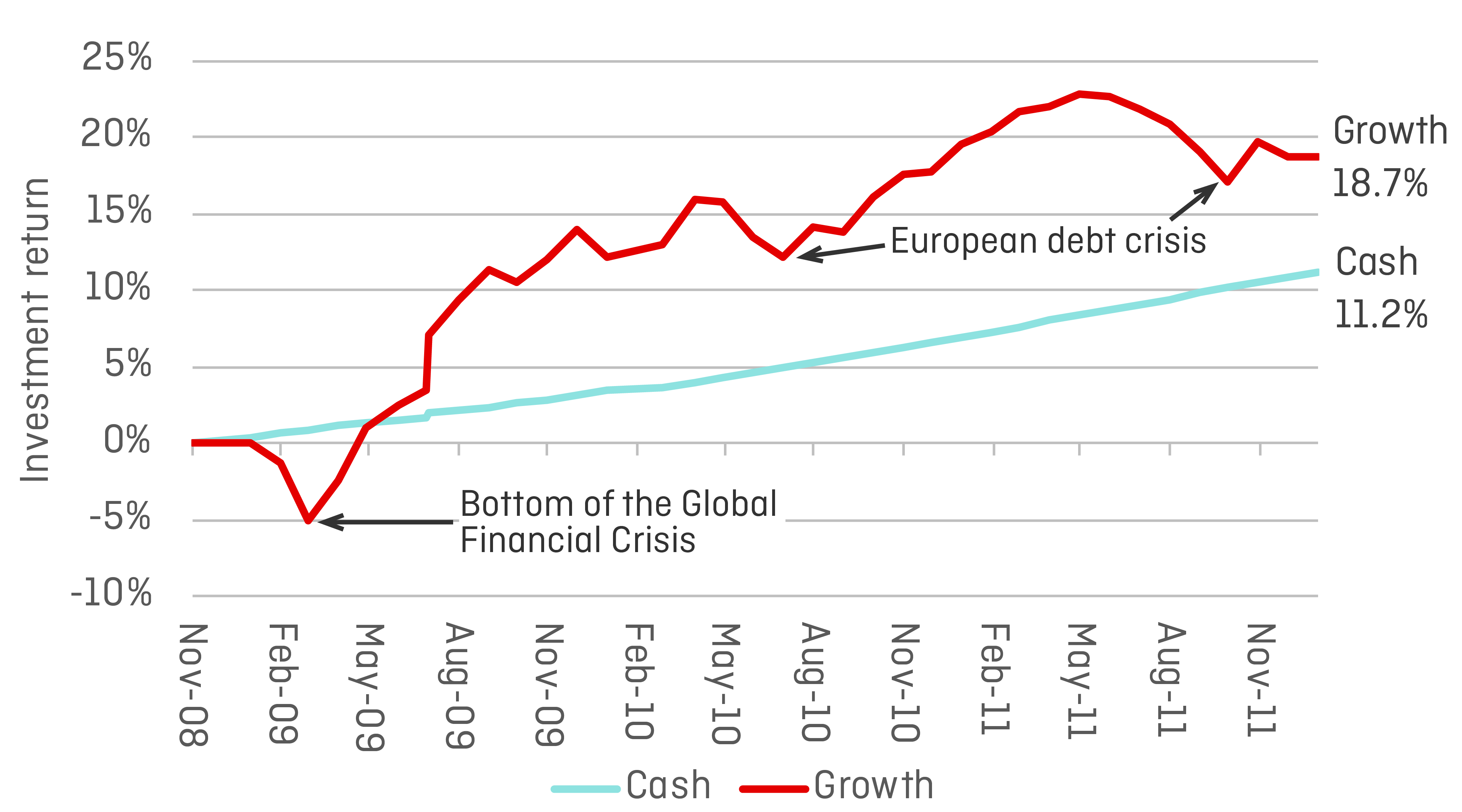

With this in mind, we can see in the chart below the effect that switching from Growth to Cash in December 2008, which was on the way to the bottom of the market during the Global Financial Crisis, would have had on a Qantas Super member’s returns.

The chart below shows investment returns after fees for Qantas Super’s Growth and Cash investment options for the period December 2008 to December 2011.

The returns shown may differ slightly from individual returns. The actual investment return for your account will depend on the period of time you were invested in an investment option, the timing of transactions in and out of your account, and the impacts of compounding. Past performance is not a guarantee of future performance.

While this member would have benefited in the short term as markets continued to fall over the next few months, they would have missed out in the medium to long-term as markets recovered.

Though there were a few hiccups on the road to recovery in the form of the European sovereign debt crisis, the Growth option generated stronger returns over the three years to December 2011 than the Cash option.

While no one can predict where the bottom of the market is, when the rebound will kick off in earnest, or whether there will be another dip, it’s important to remember than changing your investment strategy for even a short period can have a significant impact on your long-term outcomes.

Rather than selling, Chris explained that long-term investors often see times like this as an opportunity to find deals, and invest more in high-quality assets at a lower price.

“This is just a moment in time, and quality assets are going to bounce back. There’s a lot of fear at the moment, but now is a time for courage, not fear,” Chris said.

“It’s important to look at the bigger picture in the world. Once the pandemic is over, we’ll still have consumers who want to consume – people will want to go to restaurants, be entertained, and travel.”

As we wait for markets to start their recovery, there are a few things you can think about depending on whether:

You can now subscribe to receive emails from us that suit your interests. From deep dives into the world of investments, to hot tips on getting the most out of your super, there’s a super topic for you!

Qantas Super had a strong end to the 2023 calendar year, with each of our investment options posting strong gains over the December quarter.

Markets kicked off the 2023 calendar year on a positive note, with each investment option almost doubling their return for the year to date from the December 2022 quarter to the end of March 2023.

After several years of volatility in investment markets, with returns swinging from negative to record highs, and back to the low single-digits, the 2022/23 financial year has seen a return to what we could consider more ‘normal’ numbers, with Qantas Super delivering strong absolute returns across all investment options.

If you want to learn more or need help with making a decision about your super, you can get simple advice over the phone. It’s included as part of your membership so there’s no extra cost.